Alternative Payment Models, Teeth, and Tires

Does the provider lose money making repairs, or does he make money?

Photo by ccPixs.com

There is a lot of talk in health care these days about paying differently for services. Like any other industry, we have our jargon: fee for service (FFS), pay for performance (P4P), bundles, capitation, population payment. All of this is confusing for the average American, and understandably so.

But no matter what we call it, there is a big difference between various ways of paying for health care. It’s actually not that different from how we buy stuff in other parts of our lives. This came home to me recently when my wife was in two situations:

- First, when she recently went to a new dentist to get a teeth cleaning, the dentist did a thorough exam. She then offered that if Marti wanted it, she would be happy to drill out some old fillings to see if they were likely to fail soon. Only by drilling them out could she be sure that the fillings were still sound or not. If there was a problem, she could refill the cavity or replace the whole tooth with a crown. My wife had no symptoms then and still doesn’t.

- She also recently went into the local tire store where she’d bought a set of four tires a few months ago, with a warranty. There was a screw in one of the tires (we have a lot of remodeling going on in our neighborhood). The technician looked at it, and after examining the screw and removing it told her that there was no leak caused by the screw, and she was good to go. No tire repair or replacement needed.

Quick quiz: which practitioner was operating on FFS, and which one was operating on a bundled payment?

If you said the first was FFS and the second a bundle, you get a gold star. The fundamental difference is that the first proposed transaction would have resulted in the dentist getting a fee for the work, maybe over a thousand dollars if it involved a crown. The second transaction would have been covered under a warranty, and so would have cost the tire shop time, materials, and labor, but would not have generated a new payment. This is the fundamental difference between FFS and bundles or capitation. Right down to brass tacks, in fee for service, every new service draws a new fee; in bundles or capitation, some or all services don’t generate new revenue. I often think I can spot FFS behavior and capitated behavior without knowing the financial arrangement, just from how the practitioner behaves in the transaction. For example, if a shop offers to do a “free inspection”, I think you can almost always expect them to come back with a recommended purchase of something from them. This is classic FFS behavior. Conversely when someone is capitated or works under a bundled payment, they give a lot more thought to the question, “Is this really necessary, or could we watch and wait to see if it’s really a problem?”

There are big implications for our health care system in the move away from FFS to bundles and capitation. I personally favor the latter, because I think it’s just too easy for American providers to order and reorder things without consideration for the financial consequences to the payer, which is increasingly the patient himself. Even if the patient isn’t directly responsible for the bill, someone pays for it, and that usually means the collective we, whether through insurance or government programs. Most people in health care reform think this dynamic is one of the reasons we spend twice as much as most countries and get poorer results: the FFS system incents people to do more, not better.

So when you go see your provider, which do they seem more like, the dentist or the tire shop? More importantly, which do you want them to resemble more?

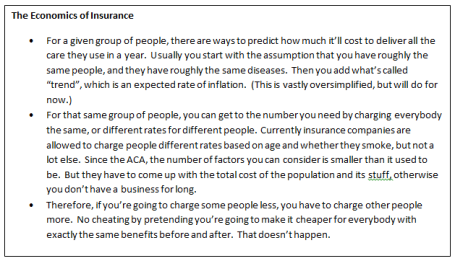

Insurance pools: how do we pay for expensive people?

Why you can’t fool all of the people all of the time

Photo by Strolic Furlan

I think for most people including me at times, the effort to repeal and replace the Affordable Care Act is an exercise in taking something they didn’t understand well but have feelings about, and replacing it with something else they don’t understand well and will have feelings about. I could comment on the state of our legislative process that this is the case, but that’s for another day and another blog.

Instead, if you can stand it, I’m going to use this column to try to explain the difficulty in reshaping the insurance pools in the ACA. First, a few rules of economics:

And one rule of insurance:

Avoid the Death Spiral: If participation is voluntary, you better give a heck of a deal to those who aren’t likely to use any stuff. They effectively make it possible for the sick people to get what they need without going broke. In the insurance biz, when you can’t attract healthy people, it’s called a “death spiral”. If all you get in the pool are sick people, you have to charge so much that you can’t sell the product to healthy people, and that makes it attractive to only those who are very sick, which makes it even more expensive, etc. You get the idea. It doesn’t end well.

The death spiral is a big deal in the insurance and policy worlds. People spend a lot of brain power trying to avoid it. Not surprisingly, Republicans and Democrats have different solutions for the death spiral. The ACA solution was called the individual mandate, which made it a taxable event to go without insurance, and therefore if you didn’t buy a policy, you put into the government kitty to make up for the risk you didn’t assume with the rest of us.

The Republican solution involves a couple of things:

- First, you allow rates to be more different than they are now. Currently in the ACA, you can’t charge anyone more than three times the lowest rate offered to someone else for the same policy. So if I’m 60 and have heart disease, I can’t have a premium more than three times my healthy daughter’s rate. Under some Republican plans, that multiple rises to five times, which is about what the market was before the ACA. But the benefit is that should make my daughter’s premium lower.

- Second, if you take a bunch of sick people out of the general pool, you can lower the rates for everyone else, because they’re no longer subsidizing all those sick people. This is a concept called “high risk pools”, and many states including Colorado had them before the ACA.

But wait, don’t the really sick people have to pay a fortune in the high risk pool to get care? The answer is yes, but in Republican solutions, the government kicks in a bunch of money to make it affordable for the sick people as well. Since the government’s money comes from all of us, we’re still subsidizing the sick, but we’re doing it through government rather than private insurance pools. (Yes, you read that right, one of the critical features of the Republican plans is government subsidies.)

Okay, what’s not to like? We avoid the death spiral because we attracted young invincibles with low rates, we give healthy people a break by taking sick people out of the pool, and we subsidize the sick in their own special off-to-the-side pool.

Yogi Berra is (wrongly) thought to have said, “In theory there’s not a lot of difference between theory and practice. In practice, there is.” When high risk pools existed before, they were chronically underfunded, and therefore really expensive for people, such that only well-off people could afford the premiums. It was a terrible slog to go to the legislature every year to ask for more money, and you can imagine what the answer was. In Colorado at least, one of the solutions was to tax the health plans, so that—you guessed it—healthy people buying insurance were effectively subsidizing sick people in a now not-so-off-to-the-side pool.

There are other ways to lower premiums for the well. You can make their policies cover less, and then the actuaries will tell the insurance companies that they can charge less and still have a business. Annual limits, lifetime limits, stripping out mandated services that don’t apply to particular individuals—all these used to exist before the ACA but don’t now, and make insurance cheaper. They may return in a future iteration of American health care.

But the fundamental rule of insurance pools is you’ve got to come up with enough money to pay all the bills. So that makes this a key question: do we want to make insurance rates for people more alike, or more different? What is the “fairest” way for all of us to pay for care through a common pool or set of pools?

Sharing: is it going out of style?

Photo by elPadawan

Back when I was in college in a small school in Indiana, I was in a fraternity, like 85% of the kids who attended there. All the guys in my house slept in one of two “dorms”, or mass sleeping rooms in the back of the house. The freshmen slept in the “rookie dorm”, and the upperclassmen slept in the other dorm (there wasn’t another name that I recall).

But over time, my fraternity brothers started building lofts, or sleeping platforms that went over their desks, for their rooms. This allowed them to sleep in their study rooms, rather than in the communal space. I’ve been back to that fraternity house in recent years, and the dorms are altogether gone, replaced by more spacious rooms that include both study space and bed space, like more traditional college dorm rooms.

Why did my friends build their lofts? The dorms dated from the mid-20th century, and looked like what was familiar to that post-war generation: barracks. It was a bonding mechanism for pledge classes, that they had to live, eat, and sleep alongside one another. Partially as a result, I still have friends from that pledge class, and I still feel loyal to them. But sharing space also meant listening to each other’s snoring, or gossip in the middle of the night.

I think about this experience now, because that drive to not have to accommodate to others is pretty human, and very American. The lofts allowed people to have their own schedules, and not have to cooperate with one another on quiet time, etc. But since then, we’ve essentially become a country where lots of kids grow up with a bedroom to themselves. But it makes me wonder if we aren’t worse off in some ways, because having to depend on and accommodate to one another made us know one another, with all our quirks and faults on display daily. (Believe me, some of it wasn’t pretty!) I wonder if in a society based on individual empowerment we aren’t losing some of the glue that holds us together in community. Freedom is great, but perhaps some experiences that force us to accommodate to one another wouldn’t be all bad. Indeed, sharing a health care financing and delivery system appears to be one of those shared experiences that will remain for the foreseeable future.

This has relevance in the ongoing debate on health care reform. Should we have community rating, or should it be experience rating? In other words, if I smoke and am obese, should I pay more for health insurance? If so, how much more? In essence, how much can and should we depend on others’ money to bail us out when we get sick? What if it’s a disease that I’m partially responsible for causing through my behavior? What if it’s something that I couldn’t reasonably prevent or control? Are there circumstances under which I don’t deserve to be able to buy insurance, because I didn’t paid into the pool when I was healthy?

As we watch a new administration unfold, these questions are going to be terribly relevant. Clearly the Obama administration’s answers to the questions above were toward the community side. Community rating, guaranteed issue, the individual mandate, and outlawing lifetime and annual maximums are all in line with the thought: “We’re all in this together. Everyone should pay into the system, and it should be there for everyone, even if you are in some part responsible for the disease from which you are now suffering.” But reading some of the Republican plans, there is more emphasis on individual responsibility and taking consequences for not living a healthy life. Which is better? The results of the past few election cycles tell me that we don’t agree as a country on the answer to this question.

MACRA proposed rules

On April 27th, CMS released proposed rules for the implementation of the Medicare and CHIP Reauthorization Act (MACRA), an act that heretofore was famous for containing the repeal of the Sustainable Growth Rate (SGR). The SGR was uniformly hated by physicians and other providers, as it theoretically controlled the rate of Medicare inflation, while in practice did nothing of the sort. It essentially put all physicians on one global cap for the nation, such that if utilization went up, the price paid for each service was adjusted down to make the overall cost effect neutral. Every year, the rate adjustment was threatened, and almost every year, some short-term, finger-in-the-dike measure was passed by Congress to avoid the cut. Providers rightly felt little motivation to think in cost-effective terms, as any efforts they made in that direction were essentially diluted by the vast majority of providers who didn’t (almost everyone else).

So this is the bargain that was struck. In exchange for getting rid of this sham spending control, providers must move to payment systems that emphasize quality and value over pure volume, through a variety of mechanisms to be determined later. “Deal!” cried providers. “Anything to get rid of the despised SGR!” But having lifted one end of that stick, the implications of the other end are become clearer.

First, there are two tracks from which you can choose as a provider. Track one is called the Merit-Based Incentive Payment System (MIPS). This is essentially a fee for service system that overlays a modifier based on several factors. These factors are an amalgam of prior incentive programs, including the Physician Quality Reporting System (PQRS), Meaningful Use, and the Value-Based Payment Modifier. There are four factors that weigh into the formula: quality, practice improvement, advancing care information, and relative cost. These factors taken together form the basis of getting paid more if you perform well, and less if you don’t. The program is designed to be cost neutral, so theoretically the bonuses paid will equal the penalties imposed. This program is intended for all those who can’t or choose not to participate in an Alternative Payment Model (Advanced APM).

The second track is the Alternative Payment Models (APMs). These include the next iteration of Medical Home, Comprehensive Primary Care Plus (CPC+); Accountable Care Organizations (ACOs); and various bundled payment programs. All of these generally share the quality of having significant financial risk for participating providers. The rewards are bigger for those participating in APMs, and probably justifiably so, as they likely involve more work and more risk financially. (Risk and reward are naturally connected, and usually commensurately so.)

This two track design carries forward CMS’ stated intent to shift to value-based reimbursement and alternative payment methodologies. It attempts to thread the needle of offering incentives for assume more financial risk, but also give credit for those who are doing good things without assuming risk. It gives some nods to small providers for whom assuming downside risk is just not feasible, given their lack of access to capital and infrastructure to bear that risk.

What will be the effect of this pivotal piece of rule-making? I would say that as of this moment, it’s impossible to tell. On the whole, it attempts to ease the transition between fee for service, still the dominant payment methodology for most payers, and forms of aggregated payment that gradually increase provider financial risk. It continues with the clear intent of moving away from FFS, and toward other payment forms that are less activity-based, and more outcome-based. It attempts to incorporate quality, interoperability, process improvement, and cost containment as determinants of payment rates, in essence saying that pure FFS alone isn’t enough to get us what we want. To get real value, you have to pay for it, and CMS is defining that value as including the above categories.

This inevitably will reshape how we practice American medicine. Whether intentional or not, this new wave of pay for reporting increases the advantage of large organizations with the access to capital necessary to track and report outcomes. It is likely, in my opinion, that it will accelerate the consolidation of the health care sector, both vertically and horizontally. The evidence that bigger is better or even just cheaper is quite mixed, and so consolidation alone cannot be the desired outcome. But it seems it may be a necessary side effect to achieve to goal of value-based care and payment.

Income and longevity

In a recent online article in the Journal of the American Medical Association (doi:10.1001/jama.2016.4226.), economists from Stanford and MIT did a very interesting thing. There is a general assumption that the richer you are, the longer you live, on average. This turns out to be true. But why does increasing income mean increasing lifespan? These economists tested that hypothesis by using two related data sources: tax returns and Social Security Administration death records. Using these two databases, they were able to map life expectancy by income level across different “commuting zones” around the country, over a fifteen year period. This involved roughly 1.4 billion tax records over that time.

The results are fascinating. Some of the conclusions:

- If you’re wealthy, geography matters less. Pretty much across the country, if you’re a man in the top 1% of income, you live to be about 87; a woman in the same income bracket lives to be almost 89.

- If you’re poor, where you live matters a lot. The difference for the bottom quartile in income is 4.5 years between the best areas of the country and the worst. This is roughly the difference we’d see in population life expectancy if we were able to cure cancer (i.e., not a small difference!).

- The study did not support four popular theories about the causal link between income and longevity.

- First, access to medical care didn’t correlate with living longer, measured by % uninsured, Medicare spending, 30 day hospital mortality rates, and use of preventive care.

- Environmental factors didn’t seem to matter. This was measured pretty indirectly, looking at the degree of income segregation in a commuting zone. The reasoning goes like this: if you have money, you move away from environmental hazard, and therefore more highly income-segregated areas would have a bigger difference between rich and poor life expectancy. Contrary to what one might expect, those regions that were more income-segregated had better longevity for the poor, not worse.

- Greater income inequality was not correlated with shorter lifespans for the poor. It was correlated with shorter lifespans for the rich. Social cohesion was not correlated with lifespan.

- Finally, local labor market conditions did not correlate with lifespan among the poor. The theory that the best thing we can do for health is to get people jobs wasn’t supported in this study.

- These were some of the characteristics that were associated with areas with higher life expectancy for the poor: higher percentage of immigrants, higher incomes, higher governmental expenditures, higher population density, and higher college graduate rates.

Well, what else correlated with increased lifespan for the poor? In addition to the factors above, they were the tried and true behavioral factors we already know about: lower smoking and obesity rates and higher exercise rates.

There is much more in this study, and I will continue to ponder its findings. But in an oversimplified way, this tells me that the best way to improve the health of communities may not be to get them more health care. The best way might be to alter the health habits of its poor. There may also be sound societal reasons for trying to clean up the environment, reduce income inequality, and reduce unemployment, but improving the health of the population isn’t one of them, at least according to the correlations found in this study.

The other thing we should notice is that this study took massive amounts of computing power. Manipulating 1.4 billion records is no small feat, but we are likely to see more studies like this because of the emergent force of big data. We should see these kinds of insights with increasing frequency as analytics get ever more powerful.

King vs. Burwell decided; starter gun goes off for insurer consolidation

In a long awaited decision, the Supreme Court of the United States handed down a 6-3 decision in favor of the administration in King vs. Burwell, a challenge to the legality of subsidies for the poor in the federal health care exchange. I am not a legal scholar, so can’t comment on the legal nuances of the case. Nonetheless, there are big implications to the law standing that even I can understand.

What this effectively means is that one of the biggest remaining legal challenges to the Affordable Care Act has failed. Future efforts will be harder, including the continued drive of Congressional Republicans to repeal and replace the ACA altogether. Most observers believe that reversal of the ACA became substantially less likely with this decision.

Some of those observers are major health plans, who shortly after the decision was handed down, announced mergers with, or acquisitions of, their peers. Aetna has announced a $37 billion purchase of Humana, and Anthem has offered (and had rejected) a $47 billion price for Cigna. The reason for the timing is that these insurers wanted to make certain that their government lines of business were stable prior to purchasing the membership of their cohorts, i.e., there would be no rollback of the millions that got new coverage as the result of the ACA.

In my last post, I discussed the incentives for providers to consolidate with one another, and with payers. The reasons for this aren’t solely or even predominantly due to the ACA, although some say that the ACA accelerated that trend. The main reason, in my opinion, is the same one I cited in the post about provider consolidation: big gets you economies of scale. That is, to build a claims processing system, or a care coordination program, or an advertising campaign for the first customer is enormously expensive. But adding the ten millionth customer? Effectively the cost is zero. Computerization has made that number even closer to zero, as you don’t necessarily even have to hire any more people to process that ten millionth customer’s enrollment or claims, just add a little more cheap computing power. Posts I have been reading since these mergers announcements talk about health insurance becoming a commodity, in which there are scarcely any product differentiators. This leaves only one basis for choosing one company over another: price. This is already the prevailing view on the exchanges, that share is predominantly determined by price, as the offerings don’t differ much between companies.

So overall, is this good or bad for consumers? On the one hand, some say that bigger health plans means less cost per enrollee due to the economies of scale just discussed, and that the mandatory medical loss ratios built into the ACA mean that the savings that result are often passed on to the consumer. Others warn, though, that consolidation reduces competition, and allows oligopolies to raise prices without the threat of being undercut by smaller and hungrier competitors. Providers in particular are loathe to face bigger and bigger insurers, even as they consolidate to gain more market leverage of their own. Time will tell, but the incentives are undeniable: big is in, on the insurer side as well as the provider side, and it’s based on pretty simple economics.

Five things I think I think about how the health care delivery system is changing

I have the opportunity to speak to a number of provider groups in the course of my work, and many recently have asked about the big picture of how care is changing. Here are some of my answers:

• Getting bigger is in. The current dynamics favor larger entities. Despite our Marcus Welby mental ideal, the facts on the ground favor large entities that have access to capital (i.e., availability of money). Modern American health care delivery is very different from the Marcus Welby days. Then, one could convert the front parlor of a house into a waiting room and a back room into an exam room, hang a shingle, and voila! You had a doctor’s office. These days, it takes a lot of infrastructure, including an electronic medical record, computers, billing software, etc. to set up the same office, and all those things cost money. If you can have several providers sharing that infrastructure, it gets cheaper per provider. More than that, being competitive in the new market means understanding one’s performance precisely, and improving that performance continually. Understanding performance and improving it also takes time and money, and it’s disproportionately expensive for small providers to do so. This means large groups and institutions that can invest in their own infrastructure on a long-term basis have an advantage. There is some irony in this, as there is some literature that says the practices that are most successful in creating high quality care at a low price, are small. But nonetheless, the capital-intensive environment that is American health care in 2015 favors big.

• Vertical integration is in—again. After a couple of waves of integration between doctors and hospitals and then subsequent waves of disintegration, it looks like this one is more likely to be permanent. Statistics show that more physicians now work for large integrated systems than those that remain independent. Accenture, a large consulting firm, estimated that in 2013, only one in three physicians remained independent. Physicians employed by larger entities are now the majority, and a growing segment of the population.

• Getting closer to where patients are, is in. One of the anomalies of medicine vs. other goods and services in America is that people still have to drive somewhere and often wait to obtain those services. Think about how other goods and services have evolved. Much of our consumer economy has migrated to the Internet, through Amazon, eBay, and other online retailers, where customers shop at their own convenience rather than during “store hours”. Amazon is up, Sears is down. Some entrepreneurs are following this model and bringing health care closer to where patients are already. We haven’t quite gotten to health care being delivered predominantly over the Internet, but we’re trying to get closer to the customer nonetheless. Evidence of this trend: CVS has just agreed to acquire Target’s in store clinics and pharmacies for $1.9 billion. And why not? People were going to Target anyway. Why shouldn’t you be able to pick up a flu shot where you buy sneakers or milk? The key is offering your services where people are going to be anyway, rather than forcing them to make a special trip to access what you have to offer.

• In(patient) is out and out(patient) is in. Many services are migrating from the inpatient setting to outpatient, and outpatient into residential. Part of the reason is cost, but there are other forces that favor this. One is the continued mass customization of our society. A recent commercial says, “Sort of you isn’t really you.” Why should consumers settle for a standard product when it can be customized to them? This is getting cheaper by the day as computers make this mass customization inexpensive and easy. A business card company advertises that it can print hundreds of business cards for you, each with a different image on it. So why should my hip replacement be done in a hospital when it can be done safely, closer to home, and more cheaply for me as a low-risk patient at a surgical center? The hospital is still there for the high-risk patient if need be, but there’s no reason to waste all that high-tech shininess (and cost) on someone who doesn’t need it.

• Quality is getting customized, too. Part of the problem of buying value in health care is making it relevant to the individual purchaser. We have very broad and general measures, but few of these speak to the average patient. How do other industries handle this? By surveying and adjusting services endlessly. By doing so, they evolve from a general definition of quality to one specific to each customer. I use a travel site to plan all my trips, business and leisure alike. Recently the website started showing me hotel picks that are selected “just for me”. What they are doing in the background is taking my past search parameters and applying them to new cities I visit. If I booked a midrange, quiet hotel in the center of the city the last few times, that’s what the program will look for in the next city. Health care is a little harder because we access it episodically and with widely varying intensity, depending on our health needs. Despite this, it is possible now to predict much more precisely what services are more likely to be satisfying to individual patients through the power of big data. The upshot of this is that the power to predict quality and satisfaction is migrating from institutions (e.g., NCQA certification) to crowd-sourced individuals who are more and more empowered to find information relevant to them individually, and contribute their own experience to the pool for the next customer.

These five trends mirror what has happened in other industries over the past couple of decades. Sellers get larger and more comprehensive to relieve the consumer of the burden of putting together a satisfying experience on their own. Buyers get more discriminating as sellers put together more satisfying products through customization. As what sellers offer gets more satisfying, our tolerance for less-than-satisfying services and experiences goes down. Such is the endless cycle of improvement that free markets foster.

The upshot of this is that it is no longer enough to offer services; those services have to be fine-tuned to the potential customer, offered at times and places convenient to that customer, and then executed expertly to produce a good outcome at a good price, within a good patient experience.

Back from the Second Annual Summit on Transparency; What’d I Learn?

In case you missed it, last week was the Second Annual Transparency Summit in Washington, a fabulous wonk sprint of two and a half days on all things transparent and emergent in health care transformation. While these conferences are always biased toward the true believers of the concept in the conference title, I left with a number of insights:

• Transparency of what, and to whom? While we tend to think of transparency as consumer information, just as critical is transparency of measurement and judgment for providers. My friend Michael Van Duren from Sutter likes to say, “In what other situation would you tell an employee, ‘your performance is bad. Fix it, despite the fact that neither you nor I have any idea how.’ That constitutes employee abuse, and it’s exactly what we do with physicians when we give them feedback most of the time.” We need more transparent and actionable information to providers to drive real delivery system change, the kind that Michael gives to his docs at Sutter all the time.

• Most at the conference agreed that increasing transparency in an opaque market is one of the reasons we should hope that health care reform might be effective. But as we teased out the nuances, it dawned on many of us that likely transparency is going to be necessary but not sufficient. The “last mile problem”, translating information into knowledge that drives action by both consumers and providers, may be emerging as the bigger, hairier human behavior problem twin to the technical problem of data massage into information. There were many examples during the conference. In one breakout session, my OB friend Neel Shah told the audience that studies show that most women want more information, but very few actually seek it out and use it in their conversations with providers. A patient spoke eloquently on the subject in the same session: “Patients don’t have the provider’s knowledge, so don’t know what to dignify in the room by asking about it. They fear looking stupid, and so they don’t ask. But what you don’t know is, while you can’t measure how I feel, it is the most important thing to me once you tell me I have a serious illness.” Even if we make clinical information more transparent as we are doing, what do we need to do to correct for the traditional sociologic factors that stifle real dialogue at the point of care?

• A fascinating emergent area, sorely needed, is patient-generated data. Prior to the conference, I thought of that mostly as people stopping to enter something on a kiosk after a clinical encounter, or responding to a survey online like you might do after a plane flight. What speakers at the conference were saying, though, was that much more data is going to be generated passively by patients through the onboard computers they carry on their phones. In addition to getting the subjective sense of an encounter through satisfaction surveys, much more info may come through Fitbits and Apple Health apps that monitor multiple personal factors automatically, without conscious thought by the individual. The metaphoric stick figures we draw right now may become much more sophisticated representations in the near future. The additional pixels to take them to high-definition will come through this automated data generation. In retrospect, this seems so obvious. Anything that requires my attention span is limited by that span’s availability. Competition for that commodity goes up daily. Much easier to get data where the only thing I have to do is walk around with my smartphone.

• Population health or individual experience? Answer: yes, and yes. While we are quite focused on population health these days, this concept can very easily and unknowingly become a goal opposed to individual experience. Fellow panelist Dominick Frosch described such an example. When we demand that patients come in for a screening colonoscopy as the only option to reduce colon cancer risk, we may scare off a significant percentage of the population who would do a stool test that is inferior as a screen, but is still way better than nothing. What we may not recognize is that the way we measure adequate colon Ca screening may dictate that rigid provider approach: if she doesn’t get the colonoscopy done, the primary care provider gets “dinged” in her system or health plan for not doing an adequate screen. And yet it’s what an informed patient, weighing her individual risk and benefit, has chosen for herself. In the future, metrics may become more mass customized to individual risks/characteristics/benefits/preferences. Why? Because computers allow us to do so, and individuals demand it be so in an increasingly mass customized world.

Finally, the most important transparency may be transparency of humanity. What became painfully obvious over and over again during the conference is people can’t hear and use any of the flood of information coming their way until they trust the people in the transaction. Whether that’s a routine office physical in which a provider offers a screening colonoscopy, or a crash situation after a major motor vehicle accident injury, feeling some common humanity between providers and patients is critical to the real dialogue many of us feel is at the core of value-based decision-making. A friend who is a cancer survivor once told me, “what I needed in a provider is someone who could say, ‘in your situation, this is the option I would choose with the least regret.’” We all crave to be cared for when we cannot care for ourselves by people who recognize and address our humanity, and share theirs with us. This desire is embedded in us deeply, in areas of the brain far below conscious thought, and it is these same areas that rule our behavior in important decisions. Allowing ourselves to be human as providers and patients together gives us the best chance to choose wisely, and live without regret. I’d say those are two really worthy goals.

The Institute for Healthcare Quality, Safety, and Efficiency at the University of Colorado Hospitals

I recently attended a graduation of sorts, from something called the Institute for Healthcare Quality, Safety, and Efficiency at the University of Colorado Hospitals. What I saw was dozens of people organized into several teams. Each team was from a different hospital unit, and each team had a project to improve quality, safety, and efficiency for its respective unit. They had used Lean and other methodologies to identify root causes, implement changes, and measuring the effect of those changes. If you’re from another industry, none of this sounds at all unusual. If you are from health care, you recognize that this is terribly unusual. In fact, this was only the second graduating class for the Institute.

Such training is old hat in many other industries, especially manufacturing. A friend who runs a health care systems engineering school tells me that one of the reasons he’d shifted into health care is that traditional industry is saturated with process improvement engineers, and there are no new opportunities for his graduates there. However, the use of industrial engineering methods in health care is relatively recent, particularly on the scale to which IHQSE aspires for its institution.

There are many possible reasons for this slow adoption, but some would argue that one of them is that process improvement hasn’t been profitable in health care under current payment systems. It simply doesn’t fit with the business model. If one is paid for activity, reducing activity through improved efficiency reduces revenue. So why would a very successful business like UCH engage in revenue reduction on any significant scale?

It’s a critically important question. A basic tenet of Clayton Christiansen’s work at Harvard Business School is that only rarely do institutions that succeed under one business model participate in the development of the one that disrupts and replaces that model. The temptation to resist change and perpetuate the last successful revenue model is just too great in most instances. And yet, that’s essentially what a hospital accustomed to being paid fee for service does when it engages in process improvement.

Likely several things are going on. It’s hard to argue with reducing harm the system does to patients. But that’s always been true, and it doesn’t explain why we did so little before, and why programs like IHQSE are now proliferating around the country. The number of financial penalties for system failures is also increasing steadily, like nonpayment for readmissions and obvious errors, like wrong side surgery (e.g., operating on the left leg when it’s the right that needs fixing).

But I hope a larger shift in thinking is happening, and that it’s good for the system and its patients. I think it may finally becoming orthodoxy in American health care that the seemingly endless stream of dollars that financed its expansion over the past couple of decades, is coming to an end. In a restricted top line growth environment, profitability increasingly depends on efficiency. And so I hope what we are watching is health care adapting to an emerging environment where efficiency and efficacy isn’t just the right moral thing to do for patients, it’s the best business model. Payers and purchasers are starting to change from paying for activity to paying for outcomes at a set price and a set quality standard. In that environment, it makes all kinds of business sense to do things effectively and efficiently, because it reduces waste, waste that the seller of the service pays for, not the buyer.

I dearly hope this is true. One of the nice things about this shift, even though it puts financial pressure on providers, is that it creates a financial benefit by improving care for patients. Suddenly making care safer, more satisfying for patients, and less expensive is good business. It was very heartening to see how proud the teams were of making their care safer, better, and more efficient. They were truly excited that they could improve the way they do things, and not simply accept that some error, even some harm, was an acceptable standard. To put it more simply, it seems to feel good to do better for the people they are entrusted to serve and the institution for whom they work, simultaneously.

Lessons from Aligning Forces for Quality: Five Emerging Trends

I recently attended one of the last meetings of the Aligning Forces for Quality (AF4Q) communities, sixteen communities around the country that have been doing payment and delivery system reform for almost a decade, sponsored by the Robert Wood Johnson Foundation. I’m sure when the whole program wraps up next April, there will be a formal report on the findings and learnings. For now, here‘s a sampling of what I’ve learned.

• Payment reform is hard, and is greatly propelled by a dominant entity demanding change. When I worked in Albuquerque, reform efforts really took off when New Mexico Medicaid included participation in a payment reform pilot as a requirement for health plans doing business with them. In Michigan, Blue Cross Blue Shield of Michigan reorganized their delivery system into a series of Physician Organizations that are tasked with improving quality and controlling cost. In Cincinnati the ongoing scrutiny of large employers drives their provider community to compete on cost and quality. The theme is that both health plans and providers pay attention when a large source of their revenue demands that they do business differently.

• Providers do best when the incentives are harmonized between payers. Over and over again we heard from providers that paying attention to multiple bonus schemes and/or quality metrics from different payment sources is very difficult. If we can harmonize these incentives, there is a greater chance we can drive change at the practice level. The current Comprehensive Primary Care Initiative (CPCI) is a product of this thinking, testing whether having the same metrics and incentives across public and private payers results in greater practice level change. The whole idea is to increase the signal to noise ratio.

• Meaningful consumer engagement remains elusive. We continue to struggle with what reporting and metrics will be meaningful enough for consumers to use to choose providers and plans. Are we simply producing measures that are relevant to policy wonks but not average people? Or are the things that average people care about so diverse that we can’t create standards across the board? Is it just that most of us use the product very occasionally, and therefore don’t have an opinion until we are embroiled in a major illness or injury? These questions remain unanswered.

• Data can be very powerful, but it takes substantial work to make it relevant and useful. A number of AF4Q communities now have access to All Payer Claims Databases (APCDs), and even with that advantage, it takes a long time to get meaningful reports out of them. Fundamentally claims were intended for one purpose: to notify a payer that services have been rendered and payment was due. But pragmatically it is often still the most accessible evidence of a clinical encounter, and so we are using these data for lots of purposes for which they were never intended. This creates problems with attribution, episode definition, analysis and interpretation of the data.

• Despite the above, almost all of the hardest challenges in payment and delivery system reform are cultural and social, not technical. As much as data analysis is still in the working-out-the-bugs phase, all of it is technically possible now. The remaining barriers are very frequently political and cultural. Some entities feel these data are key to their business advantage, and are loathe to share with others, even those who consume and pay for the services in question. There is a growing awareness that such a stance is indefensible; after all, who has a greater right to the data than those who pay for the services and those who receive them? It further takes a concerted effort by those who pay and those who use to get access to what they should have anyway. Much of the push for this access is from organizations like the AF4Q communities, entities called Regional Healthcare Improvement Collaboratives (RHICs).

Has a decade of effort to reform payment and delivery been worth it? Undoubtedly there are those who wish for more progress than has been made. I am surely one of those. But nevertheless I think it has been a success—not because all the problems have been solved, but because of the kinds of problems we are working on now vs. ten years ago. Ten years ago, almost no one had an APCD. Ten years ago, no one could conceive of how bundled payments would actually work. And ten years ago, we couldn’t even hear the voices crying for true patient partnerships, not token engagement. There is plenty left to do; for a moment, though, we should pause to celebrate what we’ve done, and how much closer we are to the system we want.