Insurance pools: how do we pay for expensive people?

February 8, 2017 at 12:51 PM Leave a comment

Why you can’t fool all of the people all of the time

Photo by Strolic Furlan

I think for most people including me at times, the effort to repeal and replace the Affordable Care Act is an exercise in taking something they didn’t understand well but have feelings about, and replacing it with something else they don’t understand well and will have feelings about. I could comment on the state of our legislative process that this is the case, but that’s for another day and another blog.

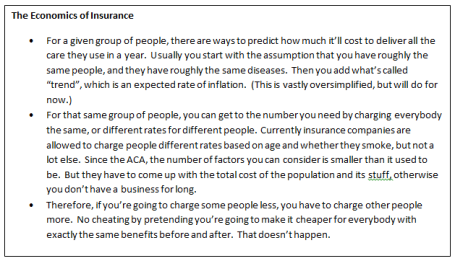

Instead, if you can stand it, I’m going to use this column to try to explain the difficulty in reshaping the insurance pools in the ACA. First, a few rules of economics:

And one rule of insurance:

Avoid the Death Spiral: If participation is voluntary, you better give a heck of a deal to those who aren’t likely to use any stuff. They effectively make it possible for the sick people to get what they need without going broke. In the insurance biz, when you can’t attract healthy people, it’s called a “death spiral”. If all you get in the pool are sick people, you have to charge so much that you can’t sell the product to healthy people, and that makes it attractive to only those who are very sick, which makes it even more expensive, etc. You get the idea. It doesn’t end well.

The death spiral is a big deal in the insurance and policy worlds. People spend a lot of brain power trying to avoid it. Not surprisingly, Republicans and Democrats have different solutions for the death spiral. The ACA solution was called the individual mandate, which made it a taxable event to go without insurance, and therefore if you didn’t buy a policy, you put into the government kitty to make up for the risk you didn’t assume with the rest of us.

The Republican solution involves a couple of things:

- First, you allow rates to be more different than they are now. Currently in the ACA, you can’t charge anyone more than three times the lowest rate offered to someone else for the same policy. So if I’m 60 and have heart disease, I can’t have a premium more than three times my healthy daughter’s rate. Under some Republican plans, that multiple rises to five times, which is about what the market was before the ACA. But the benefit is that should make my daughter’s premium lower.

- Second, if you take a bunch of sick people out of the general pool, you can lower the rates for everyone else, because they’re no longer subsidizing all those sick people. This is a concept called “high risk pools”, and many states including Colorado had them before the ACA.

But wait, don’t the really sick people have to pay a fortune in the high risk pool to get care? The answer is yes, but in Republican solutions, the government kicks in a bunch of money to make it affordable for the sick people as well. Since the government’s money comes from all of us, we’re still subsidizing the sick, but we’re doing it through government rather than private insurance pools. (Yes, you read that right, one of the critical features of the Republican plans is government subsidies.)

Okay, what’s not to like? We avoid the death spiral because we attracted young invincibles with low rates, we give healthy people a break by taking sick people out of the pool, and we subsidize the sick in their own special off-to-the-side pool.

Yogi Berra is (wrongly) thought to have said, “In theory there’s not a lot of difference between theory and practice. In practice, there is.” When high risk pools existed before, they were chronically underfunded, and therefore really expensive for people, such that only well-off people could afford the premiums. It was a terrible slog to go to the legislature every year to ask for more money, and you can imagine what the answer was. In Colorado at least, one of the solutions was to tax the health plans, so that—you guessed it—healthy people buying insurance were effectively subsidizing sick people in a now not-so-off-to-the-side pool.

There are other ways to lower premiums for the well. You can make their policies cover less, and then the actuaries will tell the insurance companies that they can charge less and still have a business. Annual limits, lifetime limits, stripping out mandated services that don’t apply to particular individuals—all these used to exist before the ACA but don’t now, and make insurance cheaper. They may return in a future iteration of American health care.

But the fundamental rule of insurance pools is you’ve got to come up with enough money to pay all the bills. So that makes this a key question: do we want to make insurance rates for people more alike, or more different? What is the “fairest” way for all of us to pay for care through a common pool or set of pools?

Entry filed under: Uncategorized. Tags: #ACA #insurance pools, #healthcare reform.

Trackback this post | Subscribe to the comments via RSS Feed