Archive for February, 2017

Undoing American Healthcare

Why assuming we’re rational about health care may be a dangerous assumption

Photo by Torbakhopper

I am reading a wonderful book called The Undoing Project by Michael Lewis, about the development of behavioral economics by two of its pioneers, Daniel Kahneman and Amos Tversky. One point of their work over five decades is that while we think we make decisions rationally and objectively, in actuality our thinking and valuation of things are fluid, and uses different criteria with different weights at different times. For example, if I am weighing where to take a vacation trip, I might choose the beach if I’m particularly tired one day, but the mountains if I’m not. Both choices would be rational ones, but not consistent from moment to moment, and therefore seemingly illogical. Which do you want, the beach or the mountains? Make up your mind!

In health care reform there are many reforms that assume consistent values and rationality: health savings accounts, reference pricing, narrow networks. All these phenomena have in common a belief that if you have people spend their own money, they’ll rationally find the best value and shift their buying choices toward those that serve them best. But what if the perceived value of services shifts depending on my circumstances as a consumer? For example, if I am buying a health insurance policy, and at the time I’m perfectly healthy, what would I choose? Most likely I would be buying strongly based on price at that moment. If I never see the doctor, I’m not actually buying medical services at that time; more likely I’m buying relief from worry that if I get sick I’ll go broke. In that case, I’m buying the cheapest policy available that allows me to sleep at night.

And, in that same case, let’s say I get diagnosed with diabetes while holding that cheapest policy. Suddenly my priorities shift. I now want a policy that gets me all the care I need at the lowest price. I am no longer as interested in cheapness, and more interested in comprehensiveness. Will I be able to go to an endocrinologist, or even an academic diabetes center? How low can I keep my copays and deductibles and still get the best care in my mind? My focus shifts partly from what I’m paying to what I’m getting.

There are instances where market theory seems to work well. The classic is Lasik eye surgery to correct nearsightedness or farsightedness. Market proponents correctly cite the steady drop in the cost of that service. But Lasik surgery has some special circumstances attached to it:

- First, no one dies without Lasik. I could get that procedure because I’m nearsighted, but glasses have worked for me since I was 10, so it’s purely elective for me.

- There are advertisements online all the time, and I can readily get pricing and a sense of how often a given surgeon performs the procedure. (This relates to safety and likelihood I’ll get the result I want.)

- I am spending my own money because the procedure isn’t covered by insurance in most cases, so I have a natural incentive to shop around.

But me rolling into the ED after a car accident? It’s possible that none of the three conditions above apply at that time. And thus the conundrum that our thinking when we purchase insurance policies may be different than when we consume services: which do you want, cheap or comprehensive? Make up your mind!

Pundits debate how much health care is like Lasik, and how much it’s like a car accident. Is it purely elective, or is it a bolt from the blue? Can I shop for it and control costs, or am I at the mercy of the provider in an emergency? The debate rages on, and we are about to see a shift in worldview in the federal government from a belief in health care’s unpredictability to it being elective and shoppable. Which do you think health care is, mostly elective, or mostly unpredictable?

Secretary Price’s ACA Replacement Plan

Is the Price Right?

Photo by Gage Skidmore

On February 10th, Rep. Tom Price was confirmed as Secretary of Health and Human Services on a party line vote, 52-47. As such, it seems prudent to learn a bit about his plans for reshaping American health care. The good news is that there is already a document that gives us a detailed view of what he’d like to see in law: he was lead sponsor of the Empowering Patients First Act, that passed the House in 2015. The bad news is that it’s 242 pages long. So here are some important points about it:

- EPFA has many of the elements Republicans have been clamoring for during the last eight years, including expansion of Health Savings Accounts, selling insurance across state lines, association health plans, and high risk pools.

- To replace the individual mandate, there are continuous coverage provisions. This allows insurance companies to charge a premium for those who have not had recent coverage, as a deterrent to those who would otherwise wait until they’re sick to get insurance.

- To replace the Cadillac tax on especially rich health coverage, there is a limit on deductibility of health insurance for companies. While wonks will argue about the difference between these two arcane provisions, the intent and effect of them are the same. Both are intended to blunt the effect of rich health coverage on increasing utilization. This isn’t popular with some in the Republican party, but it’s in here nonetheless.

- To replace the subsidies in the marketplaces/exchanges, there are refundable and advanceable tax credits. So instead of using federal dollars to make coverage more affordable, Dr. Price uses federal dollars to make coverage more affordable. EPFA is different, however, in that while the ACA subsidies are only available to lower income individuals, everybody gets access to the tax credits regardless of income. So even the wealthy will get some federal dollars to buy health insurance.

- EPFA contemplates the return of annual and lifetime maximums. Effectively this opens the door to “running out of insurance” again, not a comforting thought but something that will make insurance cheaper for everyone else. You get what you pay for.

- Medicaid provisions are a bit vague, but speak about states needing to submit plans to insure 90% of children under government programs or commercial insurance. Notably missing are details of coverage for childless adults, a big portion of the expansion population. This leads many to conclude there might not be coverage for those folks under a Price HHS.

There are other competing Republican plans out there, and it remains to be seen how much the final repeal and replace effort resembles Secretary Price’s plan while a member of the House. But it is noted in the press that his plan is one of the more aggressive in rolling back key provisions of the ACA. Many of these same provisions appear in the draft that just came out of the House, which was drawn on A Better Way, the speaker’s plan.

Alternative Payment Models, Teeth, and Tires

Does the provider lose money making repairs, or does he make money?

Photo by ccPixs.com

There is a lot of talk in health care these days about paying differently for services. Like any other industry, we have our jargon: fee for service (FFS), pay for performance (P4P), bundles, capitation, population payment. All of this is confusing for the average American, and understandably so.

But no matter what we call it, there is a big difference between various ways of paying for health care. It’s actually not that different from how we buy stuff in other parts of our lives. This came home to me recently when my wife was in two situations:

- First, when she recently went to a new dentist to get a teeth cleaning, the dentist did a thorough exam. She then offered that if Marti wanted it, she would be happy to drill out some old fillings to see if they were likely to fail soon. Only by drilling them out could she be sure that the fillings were still sound or not. If there was a problem, she could refill the cavity or replace the whole tooth with a crown. My wife had no symptoms then and still doesn’t.

- She also recently went into the local tire store where she’d bought a set of four tires a few months ago, with a warranty. There was a screw in one of the tires (we have a lot of remodeling going on in our neighborhood). The technician looked at it, and after examining the screw and removing it told her that there was no leak caused by the screw, and she was good to go. No tire repair or replacement needed.

Quick quiz: which practitioner was operating on FFS, and which one was operating on a bundled payment?

If you said the first was FFS and the second a bundle, you get a gold star. The fundamental difference is that the first proposed transaction would have resulted in the dentist getting a fee for the work, maybe over a thousand dollars if it involved a crown. The second transaction would have been covered under a warranty, and so would have cost the tire shop time, materials, and labor, but would not have generated a new payment. This is the fundamental difference between FFS and bundles or capitation. Right down to brass tacks, in fee for service, every new service draws a new fee; in bundles or capitation, some or all services don’t generate new revenue. I often think I can spot FFS behavior and capitated behavior without knowing the financial arrangement, just from how the practitioner behaves in the transaction. For example, if a shop offers to do a “free inspection”, I think you can almost always expect them to come back with a recommended purchase of something from them. This is classic FFS behavior. Conversely when someone is capitated or works under a bundled payment, they give a lot more thought to the question, “Is this really necessary, or could we watch and wait to see if it’s really a problem?”

There are big implications for our health care system in the move away from FFS to bundles and capitation. I personally favor the latter, because I think it’s just too easy for American providers to order and reorder things without consideration for the financial consequences to the payer, which is increasingly the patient himself. Even if the patient isn’t directly responsible for the bill, someone pays for it, and that usually means the collective we, whether through insurance or government programs. Most people in health care reform think this dynamic is one of the reasons we spend twice as much as most countries and get poorer results: the FFS system incents people to do more, not better.

So when you go see your provider, which do they seem more like, the dentist or the tire shop? More importantly, which do you want them to resemble more?

Insurance pools: how do we pay for expensive people?

Why you can’t fool all of the people all of the time

Photo by Strolic Furlan

I think for most people including me at times, the effort to repeal and replace the Affordable Care Act is an exercise in taking something they didn’t understand well but have feelings about, and replacing it with something else they don’t understand well and will have feelings about. I could comment on the state of our legislative process that this is the case, but that’s for another day and another blog.

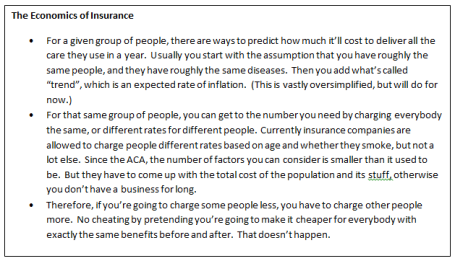

Instead, if you can stand it, I’m going to use this column to try to explain the difficulty in reshaping the insurance pools in the ACA. First, a few rules of economics:

And one rule of insurance:

Avoid the Death Spiral: If participation is voluntary, you better give a heck of a deal to those who aren’t likely to use any stuff. They effectively make it possible for the sick people to get what they need without going broke. In the insurance biz, when you can’t attract healthy people, it’s called a “death spiral”. If all you get in the pool are sick people, you have to charge so much that you can’t sell the product to healthy people, and that makes it attractive to only those who are very sick, which makes it even more expensive, etc. You get the idea. It doesn’t end well.

The death spiral is a big deal in the insurance and policy worlds. People spend a lot of brain power trying to avoid it. Not surprisingly, Republicans and Democrats have different solutions for the death spiral. The ACA solution was called the individual mandate, which made it a taxable event to go without insurance, and therefore if you didn’t buy a policy, you put into the government kitty to make up for the risk you didn’t assume with the rest of us.

The Republican solution involves a couple of things:

- First, you allow rates to be more different than they are now. Currently in the ACA, you can’t charge anyone more than three times the lowest rate offered to someone else for the same policy. So if I’m 60 and have heart disease, I can’t have a premium more than three times my healthy daughter’s rate. Under some Republican plans, that multiple rises to five times, which is about what the market was before the ACA. But the benefit is that should make my daughter’s premium lower.

- Second, if you take a bunch of sick people out of the general pool, you can lower the rates for everyone else, because they’re no longer subsidizing all those sick people. This is a concept called “high risk pools”, and many states including Colorado had them before the ACA.

But wait, don’t the really sick people have to pay a fortune in the high risk pool to get care? The answer is yes, but in Republican solutions, the government kicks in a bunch of money to make it affordable for the sick people as well. Since the government’s money comes from all of us, we’re still subsidizing the sick, but we’re doing it through government rather than private insurance pools. (Yes, you read that right, one of the critical features of the Republican plans is government subsidies.)

Okay, what’s not to like? We avoid the death spiral because we attracted young invincibles with low rates, we give healthy people a break by taking sick people out of the pool, and we subsidize the sick in their own special off-to-the-side pool.

Yogi Berra is (wrongly) thought to have said, “In theory there’s not a lot of difference between theory and practice. In practice, there is.” When high risk pools existed before, they were chronically underfunded, and therefore really expensive for people, such that only well-off people could afford the premiums. It was a terrible slog to go to the legislature every year to ask for more money, and you can imagine what the answer was. In Colorado at least, one of the solutions was to tax the health plans, so that—you guessed it—healthy people buying insurance were effectively subsidizing sick people in a now not-so-off-to-the-side pool.

There are other ways to lower premiums for the well. You can make their policies cover less, and then the actuaries will tell the insurance companies that they can charge less and still have a business. Annual limits, lifetime limits, stripping out mandated services that don’t apply to particular individuals—all these used to exist before the ACA but don’t now, and make insurance cheaper. They may return in a future iteration of American health care.

But the fundamental rule of insurance pools is you’ve got to come up with enough money to pay all the bills. So that makes this a key question: do we want to make insurance rates for people more alike, or more different? What is the “fairest” way for all of us to pay for care through a common pool or set of pools?