Posts tagged ‘#ACA #insurance pools’

Boehner says you can’t repeal and replace quickly—and he’s tried

Winning was easy. Governing’s harder.—Cabinet battle #1, Hamilton the musical

In one of the more surreal moments lately (and there have been a few), former Speaker of the House John Boehner said at HIMSS 2017 that Republicans would not be able to repeal and replace the Affordable Care Act. Here’s the quote:

The irony of this is that it was probably politically impossible for him to say that while he was Speaker. There is a scene from the Aaron Sorkin drama The West Wing in which a political consultant chides one of the characters for resolving what would have been a juicy campaign issue. “You don’t want the money, you want the issue.” The ACA was too juicy an issue to resolve in the simple manner Speaker Boehner describes, and that many of my Republican friends have been advocating for, for years. Resolving it would have removed a campaign issue that was a slam-dunk-automatic-applause-getter winner for Republicans in this last election cycle. You don’t want to resolve the issue; you want angry voters mobilized against the other guy.

But like the proverbial dog that caught the car it was chasing, it isn’t clear what Republicans can actually do quickly to unravel the complexities of the ACA. I think the ACA probably deserves a fair amount of criticism for its complexity, but then again, the issue of sustainable health coverage in the era of billion dollar medical miracles is, well, pretty complex. You want to make things affordable, but you also want to give people comprehensive coverage so they don’t worry they’ll lose everything they have in a single medical event. If you ask the American public which one they want, they’ll say, “Both, of course!” Me too. But that involves getting healthy people to buy insurance, while guaranteeing everyone can buy it, while subsidizing a fairly large segment of the population that can’t afford to be as sick as they are. Each of these aims works against the other two.

It strikes me that the hard reality of complex subjects in the nanosecond attention span world in which we live is this: it’s a lot easier in fifteen seconds to make something complex sound bad than it is to make it sound good. This is supported by a lot of neuroscience and behavioral science work in the last two decades that show that our first response to anything novel is to evaluate it as a threat, and then only when we’re sure it’s not, can we engage in rational thought. So guess which kind of problem governments typically are asked to solve?

So I don’t blame John Boehner for not saying what he said at HIMSS back when he was Speaker. After all, he didn’t make the rules, he just played the game as well as he could. The bigger question is, how do we reduce the reward for making complexity bad, and increase the reward for thoughtful problem-solving?

Is A Better Way Actually Better?

Is Paul Ryan’s world view a place we want to live? We’re about to find out.

Photo by Tony Alter

In the current debate over the Affordable Care Act’s repeal and replacement, we are watching the collision of two world views. While partisans on both sides are likely to disagree, here’s my mini sketch of each of those views:

Progressives

- Health care is a right. Everyone, regardless of ability to pay, has the right to whatever the rest of us have access to.

- The main cause of the high cost of health care is profiteering by health care companies, whether providers, pharmaceutical manufacturers, or insurance companies. If profit was eliminated and health care made a utility, it would be affordable for the average American.

- The influence of the free market should be minimized in health care, since that’s the source of that unreasonable profit in the first place. Lots of entities have made lots of money trying to avoid getting people necessary care, instead of providing it when it’s needed. That’s just wrong.

- Bigger insurance pools are better, because they are more stable, have economies of scale, and it’s easier to pay for new stuff when you can spread the cost over lots of people. The best insurance pool would be one big national pool with everyone in it. This is called a single payer solution.

- Government systems are less expensive and fairer than private systems, because there isn’t a profit in government enterprises. All that running away from expensive people that private insurances do? Government aren’t allowed to do that.

Conservatives

- Health care is a right, but it comes with responsibility, too. You should get access to care if you participate in the system. It’s your individual responsibility to take care of yourself so that you’re not needlessly draining our shared resources. This includes working to the degree possible so that you’re paying your own way as much as you can.

- The main cause of high cost in health care is overregulation and litigation. If health care weren’t so burdened by trying to prevent things that are almost never happen in the first place, and provide services you didn’t ask for, the cost would be much lower. That overregulation also stifles innovation and competition, which is what makes goods and services in this country affordable for the average person in most other industries.

- The road to restoring affordability is to unleash the power of the free market. First, make people spend more of their own money using Health Savings Accounts. Then they’ll care about the price of medical stuff, which they don’t right now because insurance pays for most of the cost. And people will only shop effectively if they’re spending their own money, not somebody else’s.

- If you truly can’t contribute to your own health care cost, we’ll give you the money to do it through refundable tax credits, and then you can shop for your own care. After all, who can shop for you better than you? Inevitably when government shops for you, they do a bad job and load a bunch of requirements and benefits in there that don’t address your individual circumstance. That’s waste, and it’s expensive.

- Private insurance is the best vehicle to cover everybody where possible. This is because private vendors respond to customer needs much more quickly and nimbly than governments can. Yes, there is profit in health care, and there should be. Why else would anyone redesign a system to make it more efficient, if they didn’t get profit as a reward? Price controls simply create more friction and waste in the market, as people will find a way to get what they want one way or another.

Who is right about this? Which world view is most true to reality? I think there are elements of truth to both points of view. But there are also a few inconvenient truths that neither side wants to acknowledge:

- For progressives, the profit in health care is a problem, but mostly they talk about that profit in drug/device companies and insurers. In fact, most of the profit in health care is in providers. For example, where are we more different from western Europe, the amount of stuff we use, or the prices of that stuff? It turns out that it’s the prices of the stuff that account for most of the cost variance. When you look at the amount of stuff we use like hospital days or doctor visits, we actually look pretty competitive vs. western Europe. This was the source of Uwe Reinhardt’s Health Affairs article in 2003 entitled, “It’s the Prices, Stupid”. Providers in our systems, whether doctors, nurses, or hospital administrators make much more than their counterparts in other countries, and that’s all loaded into the cost of insurance.

- For conservatives, the evidence that markets in health care operate like other goods is quite limited. Some will say: “Look at Lasik! Look at cosmetic surgery! You can’t tell me that medical services are that different.” They’re right, Lasik and cosmetic surgery in particular are a lot like other discretionary goods, say, the eyeglasses and make up they replace. You get to elect to use those goods or not, and you can shop for them by comparing prices for a standard, understandable service or set of services. But much of the rest of medicine isn’t that kind of shoppable service. Rolling into an emergency room, nobody comparison shops and asks to be taken to the next emergency room because of price. Then, after you start treatment, a lot of your purchasing decisions are made by your doctor, using your Mastercard (insurance) liberally. Not the price-regulating market proponents would like to see. Try this sometime: ask your doctor what a particular procedure or drug costs. Mostly you’ll get blank looks, or a reassurance that your insurance will pay for it. But actual prices, not so much.

- For everybody, the rapidly increasing cost of health care has a lot to do with our rapidly increasing ability to actually stave off death and cure stuff with technology in ways that are downright miraculous, in addition to insurance company profit and filling out forms for burdensome regulations. Stuff like being able to cure cancer or hepatitis C, or turn AIDS into a chronic disease. Would we be willing to forego such miracles to lower the cost of health care overall? Well, that depends, for many people, on whether they can see themselves having one of those diseases. If yes, then the billions spent to develop those treatments are well-spent. If you look at where the eye-popping drug costs are these days, they’re associated with just these kinds of miracles. The adult conversation we haven’t gotten to is how much of our GDP we should devote to such miracles that will benefit an unknown few of us who could be any of us, versus broad-based benefit for the many, like improving education.

It should therefore not be surprising that there is a royal disagreement in DC these days about whether/ how to repeal and replace the ACA. The ACA is founded on a progressive worldview, and the replacement will be founded on a conservative one. And conveniently, by arguing about whose view is right, we can pretend we don’t see any of the difficult issues above, and blame continuing price increases on flaws in the other guy’s theory. But if we are to get to coherent public policy, we will have to face those truths and make hard decisions as a society. Anybody on the left or the right who claims otherwise probably doesn’t have an acquaintance with these inconvenient truths.

Insurance pools: how do we pay for expensive people?

Why you can’t fool all of the people all of the time

Photo by Strolic Furlan

I think for most people including me at times, the effort to repeal and replace the Affordable Care Act is an exercise in taking something they didn’t understand well but have feelings about, and replacing it with something else they don’t understand well and will have feelings about. I could comment on the state of our legislative process that this is the case, but that’s for another day and another blog.

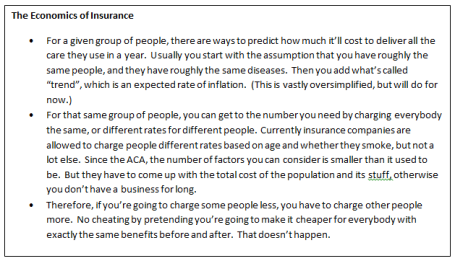

Instead, if you can stand it, I’m going to use this column to try to explain the difficulty in reshaping the insurance pools in the ACA. First, a few rules of economics:

And one rule of insurance:

Avoid the Death Spiral: If participation is voluntary, you better give a heck of a deal to those who aren’t likely to use any stuff. They effectively make it possible for the sick people to get what they need without going broke. In the insurance biz, when you can’t attract healthy people, it’s called a “death spiral”. If all you get in the pool are sick people, you have to charge so much that you can’t sell the product to healthy people, and that makes it attractive to only those who are very sick, which makes it even more expensive, etc. You get the idea. It doesn’t end well.

The death spiral is a big deal in the insurance and policy worlds. People spend a lot of brain power trying to avoid it. Not surprisingly, Republicans and Democrats have different solutions for the death spiral. The ACA solution was called the individual mandate, which made it a taxable event to go without insurance, and therefore if you didn’t buy a policy, you put into the government kitty to make up for the risk you didn’t assume with the rest of us.

The Republican solution involves a couple of things:

- First, you allow rates to be more different than they are now. Currently in the ACA, you can’t charge anyone more than three times the lowest rate offered to someone else for the same policy. So if I’m 60 and have heart disease, I can’t have a premium more than three times my healthy daughter’s rate. Under some Republican plans, that multiple rises to five times, which is about what the market was before the ACA. But the benefit is that should make my daughter’s premium lower.

- Second, if you take a bunch of sick people out of the general pool, you can lower the rates for everyone else, because they’re no longer subsidizing all those sick people. This is a concept called “high risk pools”, and many states including Colorado had them before the ACA.

But wait, don’t the really sick people have to pay a fortune in the high risk pool to get care? The answer is yes, but in Republican solutions, the government kicks in a bunch of money to make it affordable for the sick people as well. Since the government’s money comes from all of us, we’re still subsidizing the sick, but we’re doing it through government rather than private insurance pools. (Yes, you read that right, one of the critical features of the Republican plans is government subsidies.)

Okay, what’s not to like? We avoid the death spiral because we attracted young invincibles with low rates, we give healthy people a break by taking sick people out of the pool, and we subsidize the sick in their own special off-to-the-side pool.

Yogi Berra is (wrongly) thought to have said, “In theory there’s not a lot of difference between theory and practice. In practice, there is.” When high risk pools existed before, they were chronically underfunded, and therefore really expensive for people, such that only well-off people could afford the premiums. It was a terrible slog to go to the legislature every year to ask for more money, and you can imagine what the answer was. In Colorado at least, one of the solutions was to tax the health plans, so that—you guessed it—healthy people buying insurance were effectively subsidizing sick people in a now not-so-off-to-the-side pool.

There are other ways to lower premiums for the well. You can make their policies cover less, and then the actuaries will tell the insurance companies that they can charge less and still have a business. Annual limits, lifetime limits, stripping out mandated services that don’t apply to particular individuals—all these used to exist before the ACA but don’t now, and make insurance cheaper. They may return in a future iteration of American health care.

But the fundamental rule of insurance pools is you’ve got to come up with enough money to pay all the bills. So that makes this a key question: do we want to make insurance rates for people more alike, or more different? What is the “fairest” way for all of us to pay for care through a common pool or set of pools?